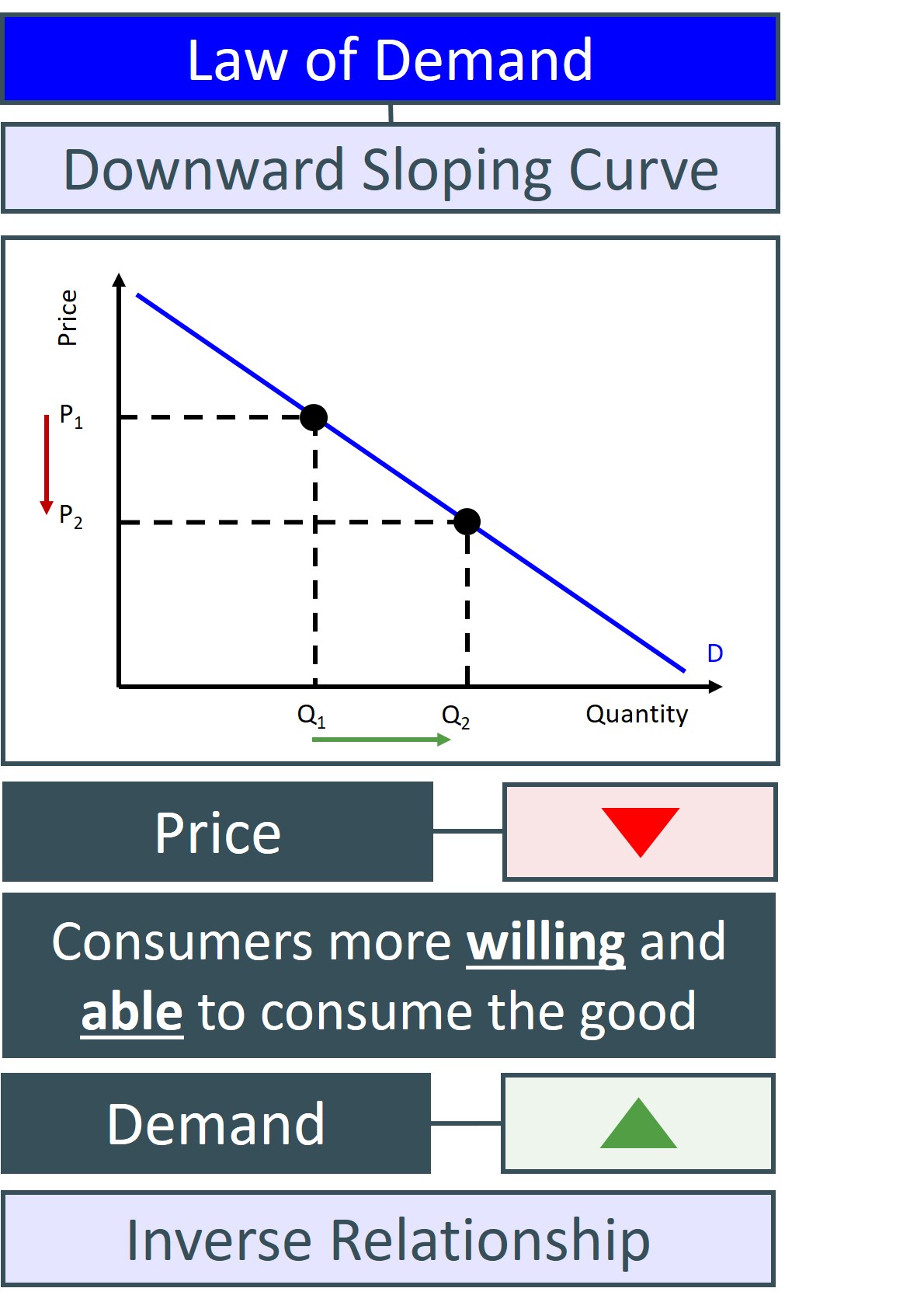

This is the theoretical explanation of why the demand curve for most goods and services is downward sloping i.e. an inverse relationship between the price of a good and the quantity demanded of that good.

This is best explained by the fact that when there is a change in the price of a good it affects the ability and willingness of individuals to consume the good at the new price. For instance, if the price of the good falls, more individuals are able to consume the good as it now fits into their affordability range. Also, some consumers that could afford the good before the price change, but were not willing to purchase the good at the original price because it was beyond their own value placed on the good, may well be incentivised and encouraged to purchase the good at the new lower price. The combined effect of these two consumption channels leads to the quantity demanded for the good or service in question to increase in response to a price fall.

The only case the law of demand does not hold for a particular good is when we are considering a veblen good. In this rare and often theoretical case, demand actually rises with the price of the good.