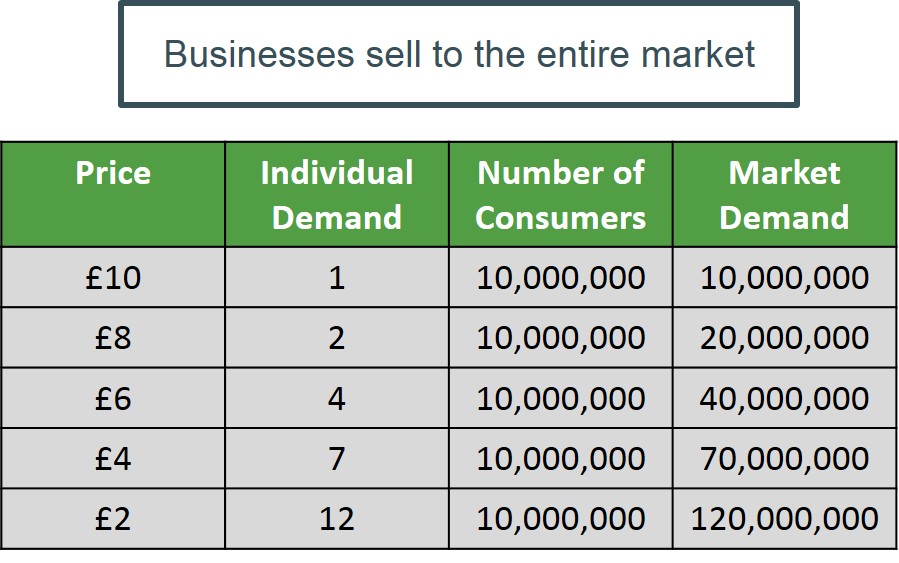

The total demand for a particular good or service i.e. the sum of the individual demand of all consumers.

Below is an example of how to derive the market demand curve. At every individual price it needs to be calculated how many consumers are willing to buy a certain amount of goods. This is shown in the table below.

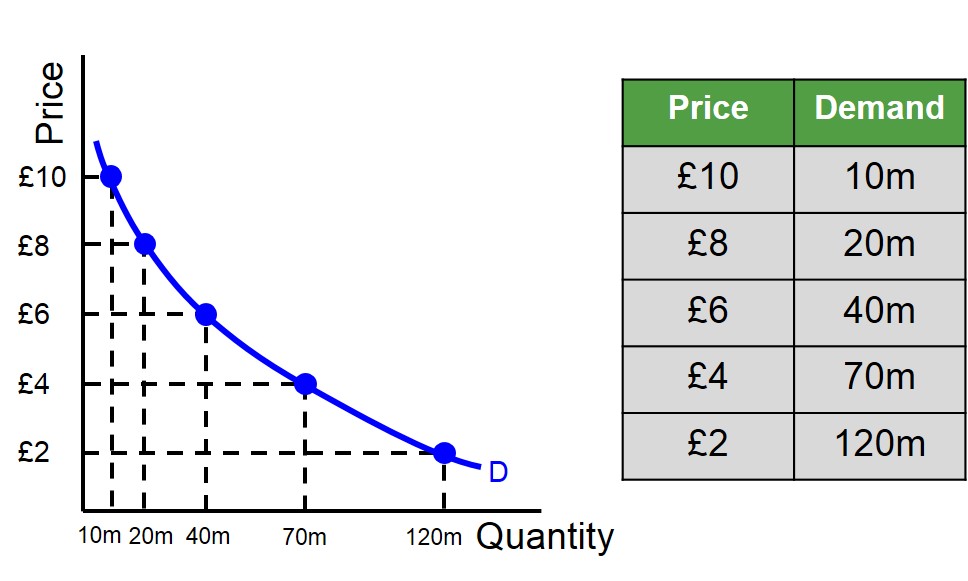

Below is the illustration of the market demand curve using the data in the table. As can be seen from the graph, the demand curve for the market has the same basic downward-sloping shape as the individual demand curve, to signify that the law of demand still holds for the market as it does for the individual demand curves.